Stop juggling, start planning

Do you know that sinking feeling when the car registration is due,

...but there is no money set aside to pay it?

Or, you have to put off buying a birthday present for someone special

...because you need to pay the bills?

Or, maybe you’ve deliberately ignored a bill

...because you know there’s not enough left in your account to cover it?

Don’t worry, you’re not alone. Many people get caught out like this.

Keep reading to learn how to plan and reduce the impact when money is tight.

What is a Spending Plan?

A Spending Planner—aka Cashflow—is a dynamic tool that predicts your income and spending. It brings your budget to life, making forward planning easy, and reducing the risk of getting caught out.

The planner shows your financial highs and lows at a glance, so you will know when money will be tight. By making adjustments, you can smooth out payments throughout the year, making your money easier to manage.

The Spending Planner is a valuable addition to your budget. While the budget worksheet and debt schedule help you gather and organise financial information, the spending planner acts as a dynamic tool, making your financial strategy practical and adaptable.

It takes a bit of time to set one up, but once it is up and running, it can be quickly and easily adjusted to suit your needs. As you become familiar with the planner, you'll gain clarity and direction for your finances—even if the journey is long, this tool provides a clear path forward.

While planning for a full 12 months is ideal, you can use the planners for shorter timeframes as well. Moni Ora worksheets, for example, offer a 12-week format to help you get started.

Creating a personal planner

Keep in mind that establishing your spending plan requires focused effort. To make your planner truly effective, take time to carefully review your spending habits and be honest about your finances. Set aside quiet time to complete this process; it may take a few sessions. Doing it thoroughly now lays the groundwork for a better financial future for you and your family.

Creating your own planner using Moni Ora's spreadsheet might seem arduous to some. After all, there are many easier online options where you can enter your details and have everything calculated and categorised directly from your bank account.

What Moni Ora offers is free downloadable tools that let you do your own adjustments, learn about budgeting functions and processes, and keep your data private. Moni Ora does not have access to your downloaded sheets.

Gathering information

The first step is to list all your income and expenses.

Download the Moni Ora budget worksheet and use it as a checklist to account for everything needed over the course of a full year.

Next, review your bank transactions over the past 3 to 12 months to ensure you capture all sources of income and all expenses. Pay attention to seasonal fluctuations or irregular spending patterns. This process provides valuable insight into your habits—often, small purchases accumulate more than expected.

Once you’ve gathered your data, use your budget worksheet to organise your spending into groups such as:

-

Weekly Expenses: Groceries, Takeaways, Lunches, Fuel/fares, Cell Phone top-up, Cash items, etc

-

Monthly Bills: Home Loan, Electricity/Gas, Phone/Internet, Pay TV, Debt repayment,s etc

-

Annual Expenses: Rates, Insurances, Vehicle expenses, School Expenses, Firewood, Memberships fees, Medical/Dentist, Clothing, Gifts, Memberships, etc

Do the math

Many people find that doing the math is an eye-opener! For instance, if you notice regular bakery purchases in your bank transactions. Add up what you've spent over a month or so, then average it out to a weekly amount. Doing the math to get an average allows for fluctuations.

For irregular spending, add up an annual total, then calculate the monthly or weekly average to determine how much to set aside to cover your expenses throughout the year.

For example, your bank transaction shows you've spent $1,000 in the past 12 months on gifts. Your average will be,

-

$1,000 ÷ 12 months = $83.33 per month

-

$1,000 ÷ 52 weeks = $19.23 per week

Knowing the numbers allows you to make an informed decision on how best to plan for these expenses. Whether it's setting aside $19.23 every week to save for gifts or adding gifts as an expense in your planner as they occur, it's up to you.

Once all the math is done and the budget worksheet is complete, you will have a clear snapshot of your current financial situation and will know whether you are overspending or have a surplus.

The spending planner builds on this by turning static budget data into a dynamic weekly plan. It helps you anticipate challenging periods and manage them proactively.

it always seems impossible

until it is done

—Nelson Mandela

Not sure where to begin?

Start with the Moni Ora Annual Expense Planner.—a straightforward tool to help you identify and plan for regular, less frequent expenses like birthdays. It’s a quick way to kick-start your journey toward living better.

For more planning tips, check out our blog: Special Occasions, Long Weekends, & Holidays.

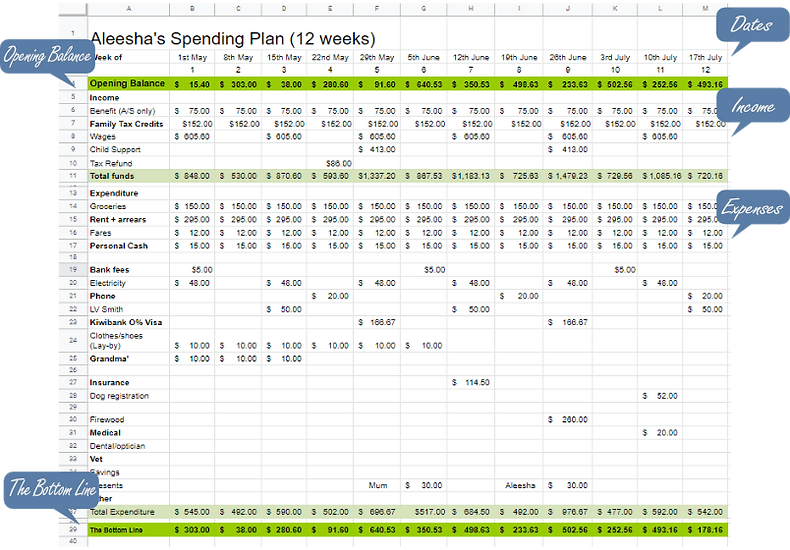

Populating the planner

Use these eight steps to set up your planner effectively. Each step includes tips to make the process smoother as you go.

Keep in mind: A 12-week planner won’t capture every expense. If a cost—like car registration—falls outside your planning window, it won’t appear. Start with a manageable timeframe and add more columns as your needs grow.

Row 2: Date

Start by entering your pay dates—weekly or fortnightly—at the top of each column so your planner matches your real income schedule. If you get extra payments (like Family Tax Credits or WINZ support), your income may vary. A weekly planner helps you anticipate these changes and stay prepared.

____________________________

Row 5: Opening Balance

In column B, enter your current bank account balance—this becomes your Opening Balance. Make sure to check your bank account(s) for the most up-to-date amount before entering it.

____________________________

Enter income

Enter your regular income for each pay period. Use the suggestions in column A as a starting point, but feel free to overwrite or remove any items that don’t fit your situation.

____________________________

Enter regular expenses

List your monthly and annual expenses in the appropriate date columns as they come due—such as power, phone, vehicle registration, or firewood. You can group similar items (like personal cash and cigarettes) if that works for you, but recording expenses separately gives you greater insight and makes it easier to adjust your plan later.

____________________________

Enter estimated irregular spending and income

Next, estimate and record any irregular expenses or income—such as gifts, clothing, or medical costs—in the columns where you expect them to occur. Including these occasional items gives you a more complete and realistic view of your finances.

____________________________

Make sure you're covered

Build in a buffer for processing delays. If you’re unsure when a payment will go through, it’s safer to enter expected income in later columns and schedule payments in earlier columns. This way, you’re less likely to risk an overdraft if a deposit arrives late or a bill is paid sooner than expected.

____________________________

Monitor the bottom line

Keep an eye on your planner’s bottom line to make sure your balance stays above your chosen minimum. This helps ensure you always have funds when you need them. If you see a minus sign (–), it means your spending exceeded your income for that period. Check the expenses in that column and make adjustments as needed.

____________________________

Your spreadsheet is NOT connected to your bank

Your spreadsheet isn’t linked to your bank account, so you’ll need to manually update it whenever your actual balances differ from your estimates. It can take a few weeks for your new planner to settle in. Review and adjust it regularly—once it’s fine-tuned, it will become a reliable tool to keep you on budget and moving toward your financial goals.

____________________________

I may not be there yet,

but I'm closer than I was yesterday - Quote

Clarify and Adjust

The core principles of budgeting are simple:

• Spend less than you earn

• Account for all income and expenses

• Plan ahead

A planner spreadsheet puts these principles into action by showing your bottom line in advance, making adjustments easier to manage. Each column calculates whether you have a surplus (income exceeds expenses) or a deficit (expenses exceed income).

A surplus means you have money left over, which carries forward to the next period. But remember, today’s surplus might be needed for future bills—not for extra spending. A deficit means you’ve overspent, so you’ll need to adjust to avoid missed payments and fees.

Reviewing the bottom line in your planner helps you see how overspending in one week can affect your finances for weeks to come. Sometimes, a deficit is delayed but will eventually drain the funds you set aside for upcoming expenses. Double-check and update your entries—especially estimates—to keep your planner practical and reliable.

Your planner’s bottom line mirrors your budget worksheet. If the budget worksheet is in deficit, your planner will be too. Don’t be discouraged; you may need to make frequent adjustments in the beginning—either to your planner and/or to your spending habits.

Keeping clear records of your actual income and spending will make future planning easier. This approach helps uncover forgotten expenses and shows where you’ve over- or underestimated amounts.

Remember, if you’re struggling to balance your incomings and outgoings, a Moni Ora Financial Mentor can help identify practical solutions. Call Moni Ora on 0800 115 370 to book a free confidential session.

Your Priorities

Once your planner is set up, you'll quickly see how valuable it can be for tracking and understanding your spending habits. As you log your spending, you can see whether your habits align with your financial priorities—or if changes are needed.

It will become clearer as to what's essential and what's optional. Missing some payments will create more problems than others, so you will need to consider the consequences of this as you go. By reflecting on these consequences, you will clarify your true priorities. Remember, your priorities may differ from others', and that's perfectly okay.

Gaining control

A personal planner gives you a clear picture of what you’ll need for regular expenses—such as living costs—and what you should set aside for irregular or unexpected costs—such as a car breakdown. Knowing this helps you decide how to handle unexpected expenses.

The more you use your planner, the better you'll get at predicting and managing life's financial twists and turns—reducing the number of 'unexpected' costs over time. You’ll feel more in control.

A Living Document

Once established, your personal planner brings your budget to life. It isn't a static document to file away and forget. You’ll need to regularly monitor it, compare it with your bank account, and update income and expenses as they happen. Always amend any amounts that differ from your estimates—this keeps your records accurate and makes your planner a reliable guide.

TIP: Check off processed payments by changing the font or cell colour in your planner to light grey—for example.

EXAMPLES:

-

If you predicted $100 for groceries but only spent $91.50, update your planner—now you have $8.50 more in your surplus than expected.

-

If you estimated a power bill at $150 but it was actually $180, update that entry so your planner doesn’t incorrectly show $30 more than you really have. Otherwise, you could overspend.

TIP: To be safe,

-

Over estimate espenses and underestimate income.

-

When using rounding, round expenses up and income down.

In the beginning, it is best to set aside a regular weekly update to check your banking against your planner for variances. Over time, you will see patterns and adjust how you do things, such as using multiple banking accounts and setting up automatic payments and transfers.

As your finances become organised, you will need less monitoring, and shorter monthly sessions might be enough. Continue to monitor and adjust regularly so your planner remains a practical tool that gives you a clear view of your finances and helps you work toward your goals.

Give it a go!

...& let us know how you get on.

Kia manahau! nā, Moni Ora